|

|

|

|

Azalia Elev. Inc.

Cash Bids

Market Data

News

Ag Commentary

Weather

Resources

|

This Dividend King Just Raised Its Payout. Should You Buy the Stock Here?

The global tobacco market is expected to reach $411.35 billion in output in 2025, supported by a compound annual growth rate of 2.37% through 2029. Traditional cigarette sales, however, continue to face pressure as regulations tighten, with the World Health Organization reporting that 6.1 billion people worldwide are now covered by tobacco control measures. At the same time, dividend-focused investors remain drawn to established tobacco companies for their steady cash flows and reliable shareholder returns. On Aug 21, Altria Group (MO) announced a 3.9% increase to its quarterly dividend, raising it to $1.06 per share from $1.02, marking the company’s 60th dividend increase in 56 years. The new annualized dividend of $4.24 per share translates into a yield of 6.3%. This move ties directly to Altria’s dividend strategy, which aims for mid-single-digit annual growth through 2028, a plan that has consistently delivered even as the industry shifts toward reduced-risk products. With regulatory pressures building and the long-term picture for tobacco still uncertain, does Altria's enhanced dividend payout and Dividend King status make it a compelling buy at current levels? Let’s take a closer look. How Altria's Metrics Stack Up Post-RaiseAltria, the parent company behind Marlboro and other smokeable and oral tobacco products, runs a business that is built on steady cash flow from its strong U.S. tobacco franchises while slowly moving into reduced-risk alternatives. That balance has supported solid stock gains in 2025, with shares climbing nearly 30% year-to-date (YTD).

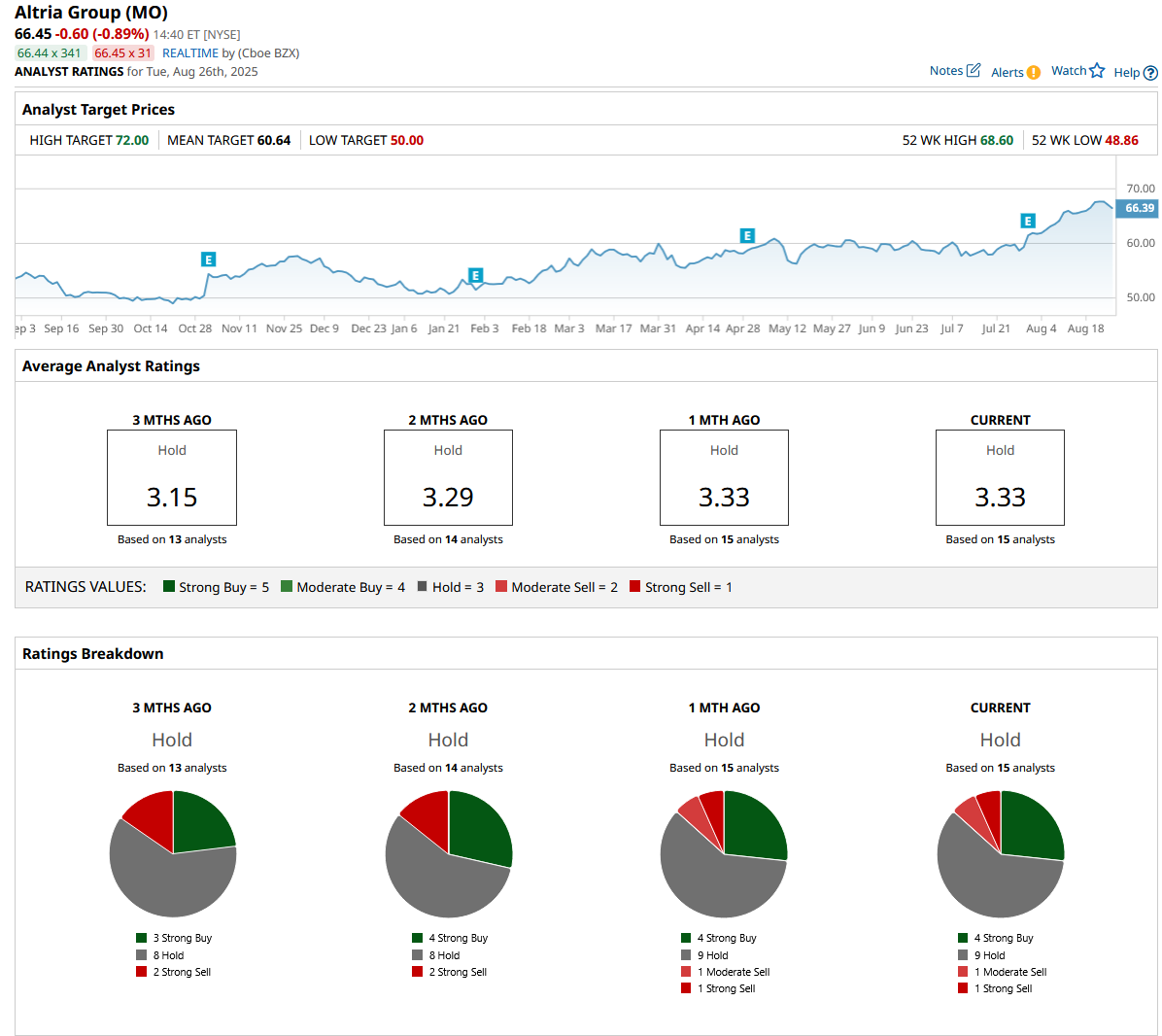

On the valuation side, MO stock still looks fairly inexpensive. It trades at a forward price-to-earnings (P/E) ratio of about 12.5x compared with the sector average near 17x, signaling modest growth without pricing in much of a premium. Financial results from 2025 tell the full story. In the second quarter, net revenues came in at $6.1 billion, down 1.7% from the prior year, mainly due to declines in smokeable products. Still, revenues net of excise taxes edged higher by 0.2% to $5.3 billion. Reported EPS fell 36.2% to $1.41, largely due to a one-time boost in 2024 from the IQOS rights sale. Stripping that out, adjusted EPS rose 8.3% to $1.44, driven by higher operating income and fewer shares outstanding. For the first half of the year, revenues declined 3.6% to $11.4 billion, but adjusted EPS improved 7.2% to $2.67, helped by efficiency gains, a lower adjusted tax rate, and fewer shares. Reported EPS for the half slipped 40.2% to $2.04, reflecting impairments and acquisition-related costs, though these did not impact the adjusted bottom line. Altria's Core Strengths and Growth CatalystsOne of Altria’s most important growth drivers is its push beyond cigarettes, and the on! nicotine pouch brand continues to gain traction. In Q2 2025, shipments increased 26.5% to 52.1 million cans, while its share of the oral tobacco category rose to 8.7%, up 0.7 percentage points from a year earlier. Inside the pouch segment specifically, on! now holds a 17.9% share, giving Altria a stronger position in one of the few parts of the industry still growing. At the same time, Altria is working on an even bigger step forward with heated tobacco. Through Horizon Innovations, its joint venture with Japan Tobacco International, the company is preparing to seek FDA approval for its Ploom heated tobacco devices in 2025. The partnership combines JTI’s device expertise with Altria’s regulatory know-how and its broad U.S. distribution system. If approved, Ploom could open up a new revenue stream by appealing to traditional smokers who have avoided e‑vapor products. These efforts matter because they strengthen Altria’s core identity as a steady dividend payer. The company has now lifted its payout for 57 years in a row, with the latest increase bringing the quarterly dividend to $1.06 per share. The yield stands at about 6.03%, supported by a forward payout ratio just above 76%, showing the dividend remains well-covered by cash flow. Analyst Views and What Lies Ahead for MOLooking ahead, management has narrowed its 2025 full-year adjusted EPS guidance to a range of $5.35 to $5.45. That represents 3% to 5% growth compared to the 2024 base of $5.19. Analyst estimates are in line with that target, with expectations for Q3 2025 at $1.42 versus $1.38 in the same quarter a year earlier, showing modest but steady progress year over year. Wall Street’s view on the stock is less straightforward. BofA Securities kept its “Buy” rating on Aug. 22, 2025, and raised its price target from $64 to $72, pointing to confidence in Altria’s smoke-free strategy and dependable cash flows. The broader analyst group, however, is more cautious. Out of 15 surveyed, the consensus remains a solid “Hold,” reflecting worries about whether declining cigarette sales will limit future revenue growth. This divide is clear when looking at price targets. The consensus mean target for the stock is $60, which is about 11% below Altria’s current price. ConclusionSo, should you buy Altria after its latest dividend hike? If you’re an income-focused investor, the case is clear: a 6%+ yield, 57 straight years of dividend increases, and resilient cash flows make MO one of the most reliable income plays around. But for growth‑hungry investors, the story is trickier. Regulatory headwinds and flat top-line growth limit the stock’s upside, and with the consensus price target sitting below current levels, analysts don’t see much room for appreciation. Most likely, shares will tread water near current highs, rewarding investors through dividends rather than dramatic price gains.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here. |

|

|